Risk Pooling Compliance.

Risk Pooling Compliance

{kind=link}

4

1. Concept and Meaning

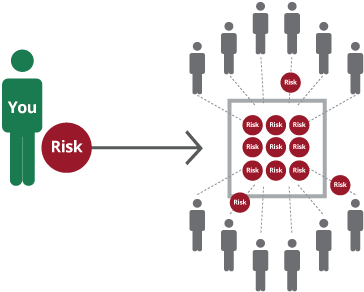

Risk Pooling Compliance refers to the legal and regulatory framework governing how risks are aggregated and shared among multiple participants (typically in insurance, reinsurance, or financial arrangements) while ensuring adherence to laws, fairness, and market integrity.

Risk pooling works on the principle that:

Many participants contribute to a common pool → Losses of a few are covered by contributions of many.

It is fundamental to:

- Insurance markets

- Health schemes

- Reinsurance arrangements

- Government-backed risk pools (e.g., disaster insurance)

2. Objectives of Risk Pooling Compliance

- Ensure fair distribution of risk and cost

- Prevent discrimination and adverse selection

- Maintain financial solvency of pools

- Protect policyholders and participants

- Ensure regulatory oversight and transparency

3. Core Elements of Risk Pooling Compliance

(a) Legal Authorization

- Pools must be created under statutory or regulatory approval

(b) Fair Contribution Mechanism

- Premiums must reflect risk appropriately (actuarial fairness)

(c) Non-Discrimination

- Avoid unlawful exclusion or biased pricing

(d) Transparency and Disclosure

- Clear terms for participants

(e) Solvency and Capital Adequacy

- Adequate reserves to meet claims

(f) Regulatory Supervision

- Oversight by insurance regulators

4. Types of Risk Pooling Structures

(i) Insurance Pools

- Multiple policyholders share risk

(ii) Reinsurance Pools

- Insurers share risks among themselves

(iii) Government Risk Pools

- Disaster insurance, crop insurance

(iv) Health Insurance Pools

- Community rating and shared healthcare risks

5. Legal and Regulatory Concerns

- Adverse Selection (high-risk participants dominate pool)

- Moral Hazard (reduced incentive to avoid risk)

- Competition Law Issues (cartel-like behavior among insurers)

- Solvency Risks (insufficient funds for claims)

6. Key Case Laws on Risk Pooling Compliance

(1) Group Life & Health Insurance Co. v. Royal Drug Co. (1979)

- Concerned agreements between insurers and pharmacies.

- Court held such arrangements were not the “business of insurance.”

- Principle: Not all risk-related arrangements qualify for insurance regulatory exemptions.

(2) Union Labor Life Insurance Co. v. Pireno (1982)

- Addressed peer review mechanisms in insurance.

- Court limited scope of “business of insurance.”

- Principle: True risk pooling must involve transfer and spreading of risk.

(3) SEC v. Variable Annuity Life Insurance Co. (VALIC) (1959)

- Determined whether variable annuities were insurance.

- Principle: If risk is borne by investor, it is not true risk pooling.

(4) Metropolitan Life Insurance Co. v. Massachusetts (1985)

- Upheld state regulation mandating minimum health benefits.

- Principle: States can regulate risk pooling to ensure fairness.

(5) National Federation of Independent Business v. Sebelius (2012)

- Examined individual mandate under healthcare law.

- Principle: Broad participation is essential for effective risk pooling.

(6) American Medical Association v. United Healthcare Corp. (2000)

- Alleged improper claims handling and reimbursement practices.

- Principle: Transparency and fairness are critical in pooled systems.

(7) Travelers Insurance Co. v. Cuomo (1995)

- Concerned hospital surcharge affecting insurers.

- Principle: Regulatory measures can shape pooling mechanisms.

7. Doctrinal Principles Emerging from Case Law

(i) Genuine Risk Transfer Requirement

- Pooling must involve actual distribution of risk

(ii) Regulatory Oversight Legitimacy

- Governments can regulate pooling for public welfare

(iii) Participation Necessity

- Broad participation ensures sustainability

(iv) Distinction from Investment Products

- If risk is not transferred, it is not insurance

8. Governance Mechanisms in Risk Pools

(a) Board or Governing Body

- Oversees pool operations

(b) Actuarial Controls

- Pricing and reserve calculations

(c) Compliance Systems

- Ensure adherence to regulations

(d) Audit and Reporting

- Financial transparency and accountability

9. Best Practices for Compliance

- Actuarially sound pricing models

- Clear eligibility and participation rules

- Strong capital and reserve requirements

- Regular regulatory reporting

- Independent audits

- Transparency in claims handling

10. Challenges

- Balancing fairness with profitability

- Preventing adverse selection

- Managing large-scale catastrophic risks

- Regulatory fragmentation across jurisdictions

11. Analytical Perspective

Risk pooling is both:

- A financial mechanism (spreading risk)

- A regulatory construct (ensuring fairness and stability)

Courts emphasize:

- Substance over form (actual risk transfer)

- Protection of participants

- Legitimacy of regulatory intervention

12. Conclusion

Risk Pooling Compliance is essential to:

- Insurance system stability

- Consumer protection

- Efficient risk distribution

The case law consistently establishes:

Risk pooling must involve genuine risk sharing, fair participation, and strong regulatory oversight—otherwise, it loses its legal and economic validity.

RELATED Blog

comments